This global trend was reflected in transactions in Slovenia. However with increases in interest rates and inflation potentially just around the corner, leading to a possible slowdown in economic activity, what are the consequences for M&A activity in the region likely to be in the coming years?

Global M&A landscape

2020 was an unprecedented year in virtually all aspects all of life, and M&A activity in the region was no exception. Of course the primary impact of the pandemic was the personal pain, disruption and loss caused by the impact on the health of so many, but the severe disruption caused by the COVID-19 pandemic also had an enormous impact on the economy. Different economic sectors were affected in very different ways, from the extremely negative (e.g. non-food retail, travel and hospitality) to the broadly positive (e.g. health and TMT). Furthermore, even at the end of 2021, supply chain issues caused by production shut-downs and logistical issues are still working their way through the economic system.

Naturally, during 2020 the uncertainties about the longer term impact of the pandemic caused investors to delay investment decisions in order to see how the new normal would look when the world began its recovery from the pandemic. Once travel restrictions began to gradually lift, and investors could make a better informed evaluation of the longer term impact of the pandemic and the measures taken to mitigate its impact, then the pent-up demand due to the lack of transactions in 2020 and the wish to align business strategies to better fit the new market landscapes came into play.

Slovenia and the region conform to global trends

In common with global trends, the CEE & SEE markets experienced significant growth in transaction numbers and average deal values from 2020 to 2021. Total deal values in the region during Q1 to Q3 rose from €23bn to €49bn with an increase in the number of transactions of 32%, and an increase in the average deal value of 61%.

As could probably be expected, the most active countries in terms of transactions during the pandemic period were Austria, Poland and the Czech Republic, but there have been some significant transactions in the Adriatic region as well, including especially several large transactions involving Slovenian entities.

- In Q4 2020 the Slovenian market received the stunning news that Bia Separations, a company which in its recent past had been on the verge of bankruptcy, had been sold for a whopping €360m to the German biopharmaceutical giant Sartorius.

- Just before New Year in 2020, NLB announced that it has successfully completed the acquisition of Serbian financial group Komercijalna banka a.d. The acquisition included the purchase of an 83.23% stake in the target company for €394.7m. This acquisition allowed the NLB group to increase its market share in Serbia by 10 percentage points, making it the third largest banking group in the country.

- Petrol announced in Q1 2021 that it had agreed to acquire a 100% share in Croatian Crodux in a transaction worth over €190m. This move cements Petrol’s position as the second largest oil and gas provider in Croatia by giving it an additional 93 gas stations there. It represents the single largest increase in sales points for the group since its inception.

- Serbian businessman and owner of Gorenjska banka, Miodrag Kostić acquired HETA asset resolution from its Austrian owners for approximately €240m in Q2 2020. The target reportedly holds over €100m of real estate and €550m of receivables, implying a significant discount on the face value of the assets.

- Gorenjska banka, together with AIK banka, signed transaction documents acquire Sberbank’s operations in the region. The deal was signed in Q4 2021 but various regulatory approvals are still pending.

- in Q2 2021 the OTP group announced that it had signed an agreement to acquire NKBM from Apollo and EBRD, making the Hungarian banking group, which already owns SKB, the largest banking group in Slovenia. This dethroned NLB from the top spot for the first time in the country’s history.

TMT remains king, both globally and in the region

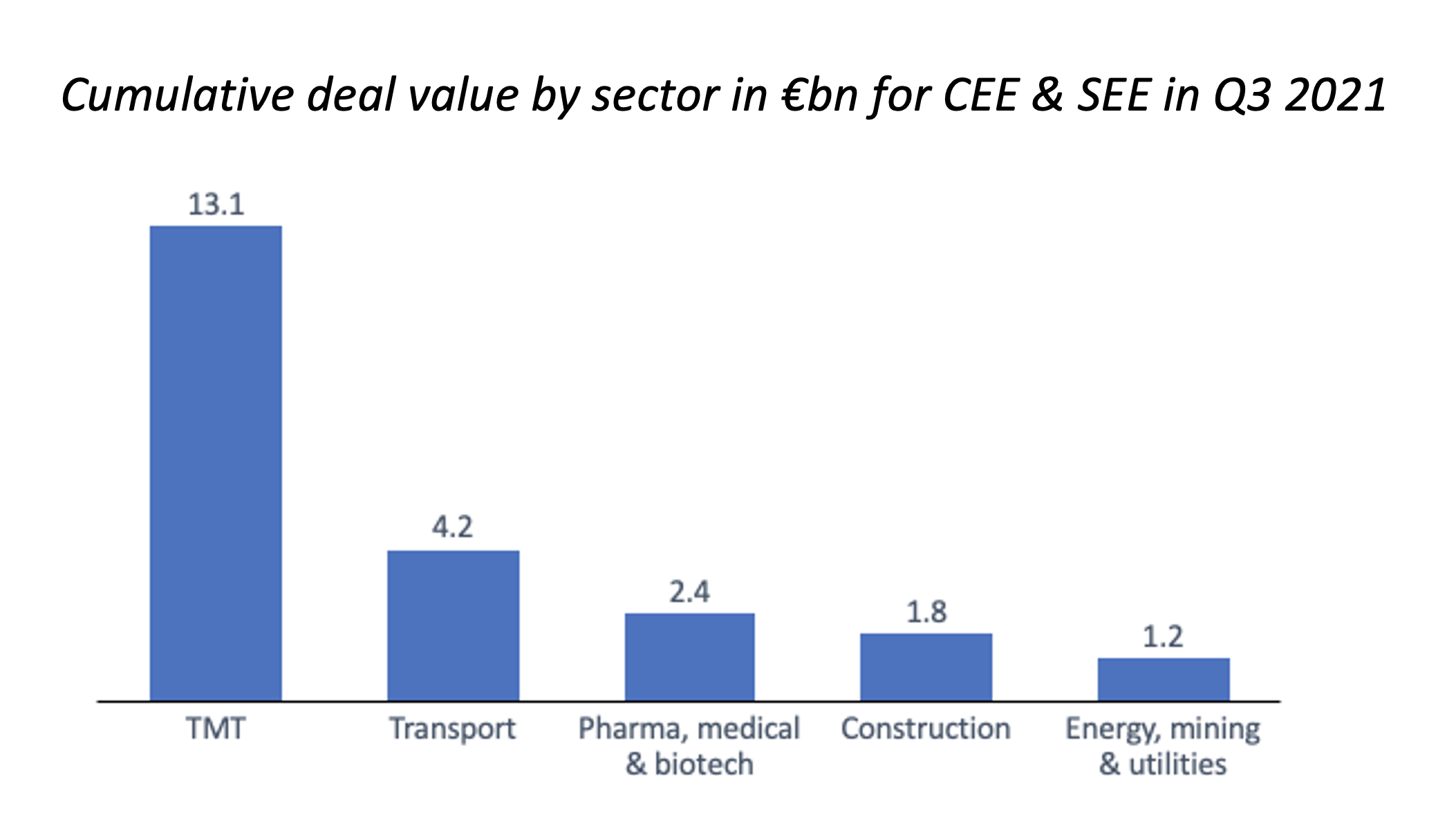

M&A activity is expected to remain strong in Q4 2021 as there are currently an estimated 566 deals in consideration in the CEE and SEE region at the moment. Deal volumes by sector are given in the following chart:

As well as being the most active sector in terms of potential deal flow, TMT was also the sector with the largest transaction values with 5 out of the 10 highest value transactions announced in Q3 2021 involved TMT companies. The cumulative deal value of the sector for the first three quarters of 2021 was €13bn, with transportation, the next largest sector by value, reaching only about a third in terms of deal value.

There are a number of factors which cause the TMT sector to be heavily represented in terms of both the number of transactions in the pipeline and in terms of the deal value. We believe that this sector is one which has benefited most from the move online caused by the pandemic. Also, in the telecom part of this sector is naturally heavily consolidated, leading to higher average transaction values.

Conclusion

In our view, the level of M&A activity is at a record high due to a number of factors. Firstly, there is a clear impact of a rebound in activity following the impact of the pandemic. Secondly, companies have examined their medium term strategies to better position themselves to thrive in the changed post-pandemic market conditions. Thirdly, the continuing historically low levels of interest rates have supported record high levels of valuation, at least for now. And fourthly, both companies and financial institutions have accumulated substantial “war chests” with which to support M&A activities. We expect that the influence of each of these factors to begin to decline in the near future, therefore reducing the level of activity and the valuations enjoyed by sellers.